Market Outlook: US Election

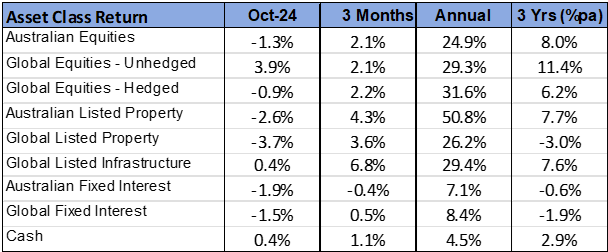

October 2024 Review: Equities pause as bond yields move higher

- Bond yields jumped sharply in the lead up to the US election.

- Equity markets recorded small losses, with listed property underperforming.

- The $A fell as some of September’s commodity price bounce unwound.

INTERNATIONAL EQUITIES

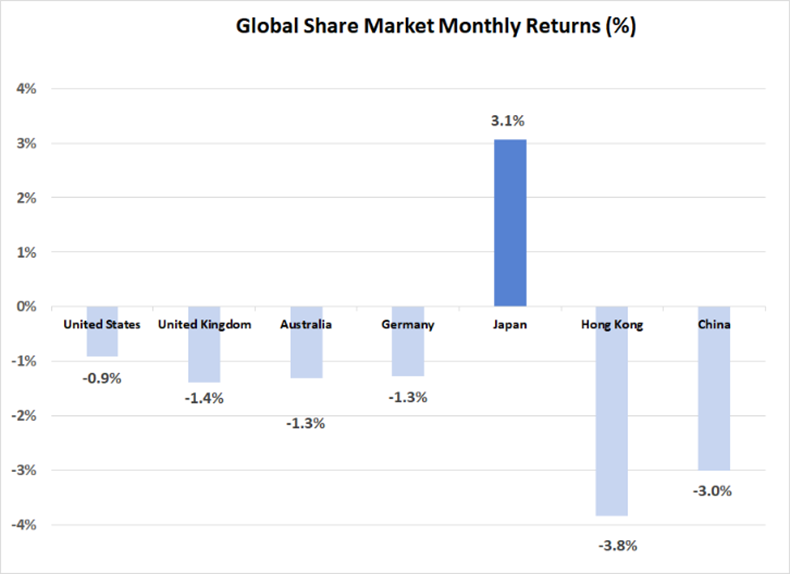

The rally on global equity markets paused during October, although the 0.9% average decline in developed markets was modest relative to the size of the increase in bond yields. This resiliency of equity markets reflects ongoing positive investor sentiment, which was buoyed last month by another generally positive quarterly US earnings reporting season. The US market moved in line with the global average, with the S&P 500 Index declining by 0.9%.

Technology stocks closely mirrored the broader market last month. Similar reductions were recorded across Europe, with Japan’s 3.1% rise being the stand-out. A weaker Yen boosted prospects for Japanese export companies, with the Bank of Japan’s announcement late in the month that there would be no change in interest rates also adding to investor confidence.

Emerging markets were weighed down by a 3.0% fall on the Chinese market last month, which followed the significant 23.2% rise in September. Although there was some disappointment that the Chinese economic stimulus program (announced in September) was not followed up by more extensive fiscal policy measures, the net appreciation of the Chinese market over the past two months has been substantial. Adding to the negative returns received from emerging markets was an 8.0% decline recorded on the Indian market, with some company earnings results disappointing investors. Higher US bond yields and a strong US currency (both of which prevailed over October) are typically negative for emerging markets, as foreign capital is encouraged to flow to the US where bond returns have become higher.

Some of the recent strength in listed property was reversed in October, with higher bond yields making the sector less attractive in relative terms. Australian listed property was 2.6% weaker, with global property down 3.7%. However, both asset classes remain well ahead on a quarterly and annual basis. Global infrastructure maintained its positive trend, rising by 0.4% to be 29.4% higher for the year. Ongoing increases in demand forecasts for US electricity, much of which is related to expected data centre use, has been supportive of the valuations of US electricity utilities, which has been a key contributor to returns in the infrastructure asset class over the past year.

AUSTRALIAN EQUITIES

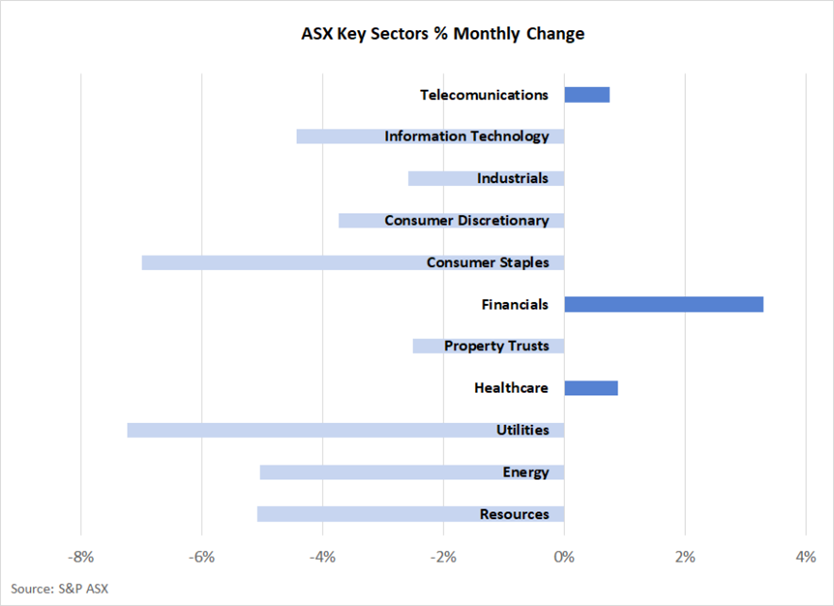

Australian equities slightly underperformed the global average with the S&P ASX 200 Index falling by 1.3%. Sector movements were very mixed, with some of September’s rotation away from banks towards resources being reversed last month. Support returned to banking stocks, allowing the financial sector to gain 3.3%, with resource stocks declining 5.1%. Weakness continued in the energy sector as oil prices remained at low levels despite the ongoing conflict in the Middle East. Energy stocks fell 5.0% over the month and are 17.2% lower for the year – making energy the weakest sector on the Australian market over the past 12 months.

Also heavily detracting from returns last month were consumer staple stocks. A weaker than expected trading update from Woolworths (down 10.0%) was the main contributor the sector’s decline. Consumer discretionary stocks were also weaker, with a 4.5% drop in Wesfarmers weighing on returns.

FIXED INTEREST & CURRENCIES

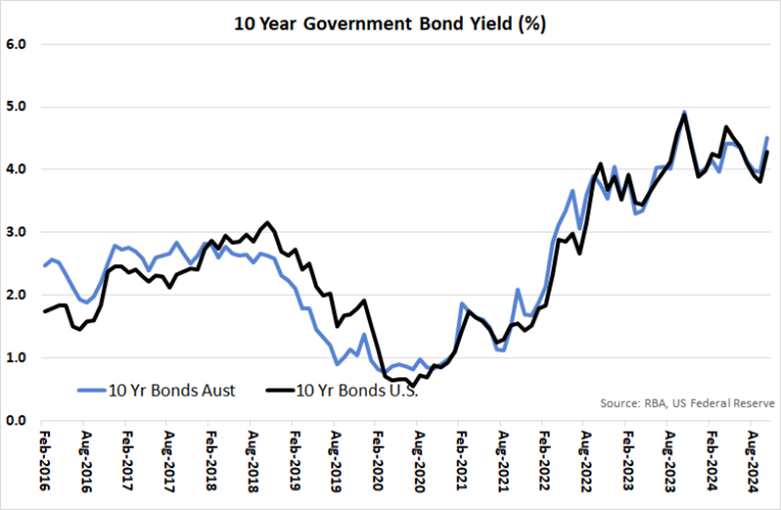

Despite the 0.5% reduction in the United States cash rate in September, and further declines in European cash rates last month, there was a sharp increase in longer term bond yields over October. The U.S. 10-year treasury bond yield jumped from 3.81% to 4.28%. Australian yields rose by a wider margin, with the 10-year government bond shifting from 3.96% to 4.52%. Higher yields appeared to be prompted by a slightly higher than expected monthly inflation result in the U.S., as well as a firming view that a Republican victory in the US election would be inflationary due to higher tariffs and increased government expenditure. Whereas Australian longer term interest rates increased, the overnight cash interest rate remained at 4.35% following the Reserve Bank’s meeting in early November. Ongoing strength in the labour market, combined with only modest declines in underlying inflation, continue create the case for the RBA to maintain existing policy settings.

Higher US bond yields were supportive of the $US last month, with the $A losing some support as commodity prices weakened following the bounce in September. As a result, the $A declined from US 69.3 cents to US 65.7 cents. The $A was also 2.5% lower against the Euro, but gained 2.3% against a weaker Yen. The broader depreciation in the $A resulted in unhedged global equity investments increasing in value, despite the underlying fall in share prices.

OUTLOOK AND PORTFOLIO POSITIONING

Current investment portfolio positioning considerations will understandably be dominated by an assessment of the implications of the Republican victory in the US election. Given the intensity of the media’s focus on the election, it would be easy to develop an exaggerated view of the election’s importance for financial markets. However, for the most part, elections, and geopolitical events more generally, rarely have long lasting effects on financial markets.

The fact that the election result has been decisive, with the result largely in line with prior market consensus, should be generally supportive for equity markets. A Republican victory implies a supportive environment for the corporate sector and removes the possibility of higher corporate tax rates. Forecast company earnings should be largely unchanged following the election, and, as such, the implications for share markets are likely to be limited. Whilst it could be argued that increased tariffs are ultimately bad for economic growth across the globe, this will take time to play out and there is a reasonable possibility that the appetite for restrictive trade initiatives will dilute over time.

As has been widely predicted, a Republican victory may result in higher inflation and higher interest rates than would otherwise be the case. Tariffs are inflationary and increased government spending can also place upward pressure on prices. Additionally, immigration restrictions and deportation could drive higher wages. To a large extent, however, movements in bond yields in recent weeks may have already taken this higher inflation into account, with equity markets absorbing this change without any major shock to valuation. A higher interest rate regime may, however, make it less likely that interest rate sensitive assets such as listed property continue their upward path.

One theme that may develop now that the election has passed is a renewed focus on the US budget deficit and the large bond issuing program that is required to fund this deficit. Despite the economy being buoyant, the US Government is running an annual deficit equivalent to 6% of the size of the economy and this deficit looks set to increase to meet pre-election spending plans. With more bonds required to be issued, the increased supply may cause bond prices to fall (and yields subsequently increased). An anticipation of this renewed focus on bond issuance may help explain the significant increase in yields that took place in October.

For Australian investors, the upward movement in bond yields over recent weeks may be the most significant election related opportunity that has been presented. Australia has a weaker growth trajectory than the US economy, with a much lower government budget deficit. As such, it could be argued that Australian bonds offer less risk than those of the US – yet are currently providing a higher yield. Longer term Australian bond yields are now higher than the cash rate and the likelihood that cash rates will fall in 2025 remains high, thereby making the margin available in longer term bonds all the more attractive.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.